When preparing to buy a home, one of the biggest factors to plan for is the down payment. The amount you’ll need depends on various factors, including the type of loan you choose.

In this article, we’ll explore how down payment requirements influence your mortgage payments and how much you might need to put down, depending on the loan option that best fits your situation.

What Is a Down Payment?

A down payment is an initial cash payment made at the start of purchasing a high-cost item, like a home or car. It represents a percentage of the purchase price and is paid by the buyer at closing.

However, the down payment isn’t the only cost due at closing. Buyers may also need to cover closing costs, which include fees for processing paperwork and finalizing the mortgage. These costs may sometimes be covered by the seller or shared between buyer and seller, depending on the terms of the agreement.

How Much Down Payment Do You Need to Buy a House?

Traditionally, homebuyers using a conventional loan aimed to put down 20% of the home’s purchase price, and some lenders still prefer this. However, with rising home prices, many buyers today—especially first-time buyers—make down payments well below 20%, even with conventional loans.

In fact, down payments can now be significantly lower, and certain loan programs may even allow for zero down. The exact amount you’ll need largely depends on the type of loan program you choose and the requirements of your mortgage lender.

What Is the Minimum Down Payment for Buying a House?

While a 20% down payment is often preferred by some lenders, the minimum required down payment can vary widely based on the loan provider and the purchase price. Down payments can range from as high as 20% to as low as 3%, depending on the loan type.

If you make a smaller down payment—or no down payment at all—you may be required to pay for private mortgage insurance (PMI). PMI protects the lender in case of loan default. To avoid PMI, buyers generally need to put down a larger amount upfront.

Advantages of Making a Larger Down Payment

Here are some key benefits of a larger down payment to consider:

Paying Less Over Time

A larger down payment reduces the total loan amount, lowering the overall cost of your home. Since mortgage interest is calculated as simple interest, it doesn’t compound, meaning the smaller the loan, the less interest you pay.

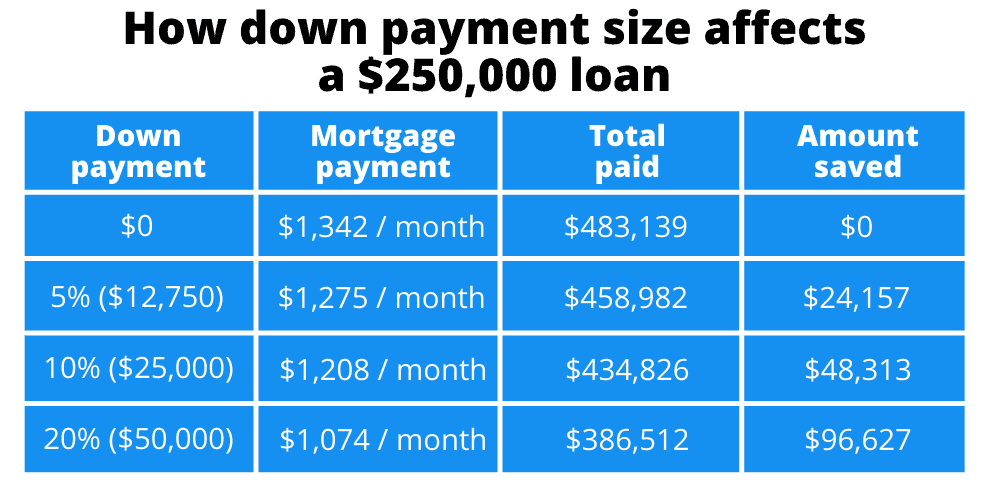

For example, on a 30-year fixed-rate loan of $250,000 at 5%, a $0 down payment would result in monthly payments of $1,342, totalling $483,139 over the life of the loan. By increasing your down payment, you could save thousands in interest. A table comparing 5%, 10%, and 20% down payments shows potential savings of $24,157, $48,313, or $96,627, respectively—a nearly 100% return on your investment.

Lower Interest Rates

Lenders are likely to offer lower interest rates when you put down 20% or more. With a larger down payment, you reduce the lender’s risk, leading to better loan terms and significant savings over the life of the loan.

Lower Monthly Payments

A larger down payment reduces your loan balance, leading to smaller monthly payments and less interest over time. For example, comparing a 5% to a 20% down payment on a $200,000 home shows how a higher down payment can significantly reduce monthly mortgage payments.

Strengthening Your Offer

In competitive markets, a larger down payment may make your offer more attractive to sellers. Sellers tend to see buyers with larger down payments as more reliable, reducing potential issues during closing. Additionally, sellers may favor buyers with conventional loans, which often require larger down payments, over buyers using VA or USDA loans that require little to no down payment.

Advantages of Making a Smaller Down Payment

Here are some benefits to consider if you’re thinking about making a smaller down payment on a home:

Getting into a Home Sooner

Saving for a large down payment can be challenging and time-consuming. A smaller down payment allows you to become a homeowner sooner, without waiting years to build up substantial savings.

Preserving Your Savings

By putting down less, you keep more funds in your savings, providing a financial cushion in case of unexpected expenses or income changes. This reserve can be useful for home repairs, improvements, or other expenses beyond monthly mortgage payments.

Remember that homeownership involves more than just the mortgage, so plan for costs like property taxes, homeowners insurance, and utilities to ensure your budget can handle these expenses comfortably.

How Much Should You Put Down When Buying a Home?

There’s no one-size-fits-all answer to how much you should put down on a home—it depends on the loan type, the home’s price, and your financial goals. Generally, most homebuyers make a down payment of 8% to 20%, though some loans may require more or less depending on loan requirements and the home’s price.

Some loan types, like jumbo loans, which exceed conforming loan limits set by the Federal Housing Finance Agency, require a minimum of 10% down. Additionally, putting down less than 20% often means you’ll need to pay for private mortgage insurance (PMI), which increases monthly payments.

When deciding on your down payment amount, consider these factors:

How Much You Have Saved

Make sure to leave yourself a financial cushion after your down payment for emergencies or other expenses. If using all your savings to avoid PMI isn’t practical, you might consider putting less down and paying PMI until you build 20% equity, allowing you to eventually refinance or remove PMI and lower your monthly payment.

How Long You Plan to Live in the Home

The longer you plan to stay, the more beneficial a larger down payment can be. However, if you plan to live in the home for fewer than 10 years, a smaller down payment may be more advantageous.

Your Goals as a Real Estate Investor

For active investors, it’s often beneficial to keep a smaller down payment to maximize cash flow for future investments. However, a larger down payment can increase equity and potentially yield greater returns when you sell the property.

The Monthly Payment You Can Afford

A larger down payment reduces your loan amount and, consequently, your monthly mortgage payment. If saving on monthly payments is a priority, putting more down to avoid PMI may be worthwhile.

Your Credit Score

Your credit score impacts both the interest rate you qualify for and, sometimes, the required down payment. For instance, FHA loans allow for a 3.5% down payment with a credit score of 580 or higher, while scores below 580 may require 10%.

How to Pay Your Down Payment

The most common methods for paying a down payment at closing include checks, money orders, or wire transfers. Some buyers consider using funds from a HELOC, 401(k), or even a credit card, though these methods are generally not recommended.

For those who can’t save enough for a down payment, there are alternatives to explore, such as receiving a down payment gift from a family member or friend. Before accepting a gift for a down payment, keep the following in mind:

Can Down Payments Be a Gift?

Yes, down payments can be gifted, but there are important legal considerations. Mortgage regulations require that the gift be documented with a letter stating the relationship between you and the giver and affirming that the funds are a gift—not a loan that needs repayment, as that would qualify as mortgage fraud.

The gifted funds should also be transferred well in advance, as lenders will need to trace the funds’ origins to verify they are legitimate. In many cases, you can receive a gift for the full down payment amount.

Are There Tax Implications for the Gift-Giver?

The person gifting the down payment may be subject to a gift tax if the gift exceeds the annual exclusion limit. For 2023, this exclusion is $17,000 per person or $34,000 for a couple filing jointly. As long as the gifted amount doesn’t exceed this threshold, no gift tax will apply.

How Much Is the Gift Tax?

If the gift exceeds the annual exclusion, the excess is deducted from the giver’s lifetime gift tax exemption, currently $12.92 million. This lifetime exemption allows individuals to give substantial gifts tax-free over their lifetimes, but going over the annual limit decreases the amount available under this exemption.

What Is Down Payment Assistance?

Down payment assistance programs are designed to help homebuyers cover their down payment costs. Each state manages its own assistance programs, which can vary widely based on the real estate market and available funding. Larger states often offer a greater number of assistance options than less-populated states.

How Do You Qualify for Assistance?

Qualification requirements differ by state and program. Some programs are tailored to specific groups, such as first responders, nurses, or veterans, while others are based primarily on income. To determine eligibility, research the programs available in your state.

Do You Need to Be a First-Time Homebuyer?

Many down payment assistance programs require applicants to be first-time homebuyers. However, according to the Department of Housing and Urban Development (HUD), a “first-time homebuyer” is defined as someone who hasn’t owned a primary residence in the past three years. For example, if you sold a home five years ago and have been renting since, you would qualify as a first-time buyer under many of these programs.

Choosing the Right Down Payment for Your Investment Strategy

Deciding how much to put down on a home involves weighing several factors to find the best fit for your financial goals and investment strategy.

With a better understanding of down payments, you’re now prepared to make a more informed choice about the loan type that aligns with your plans and the down payment it may require.